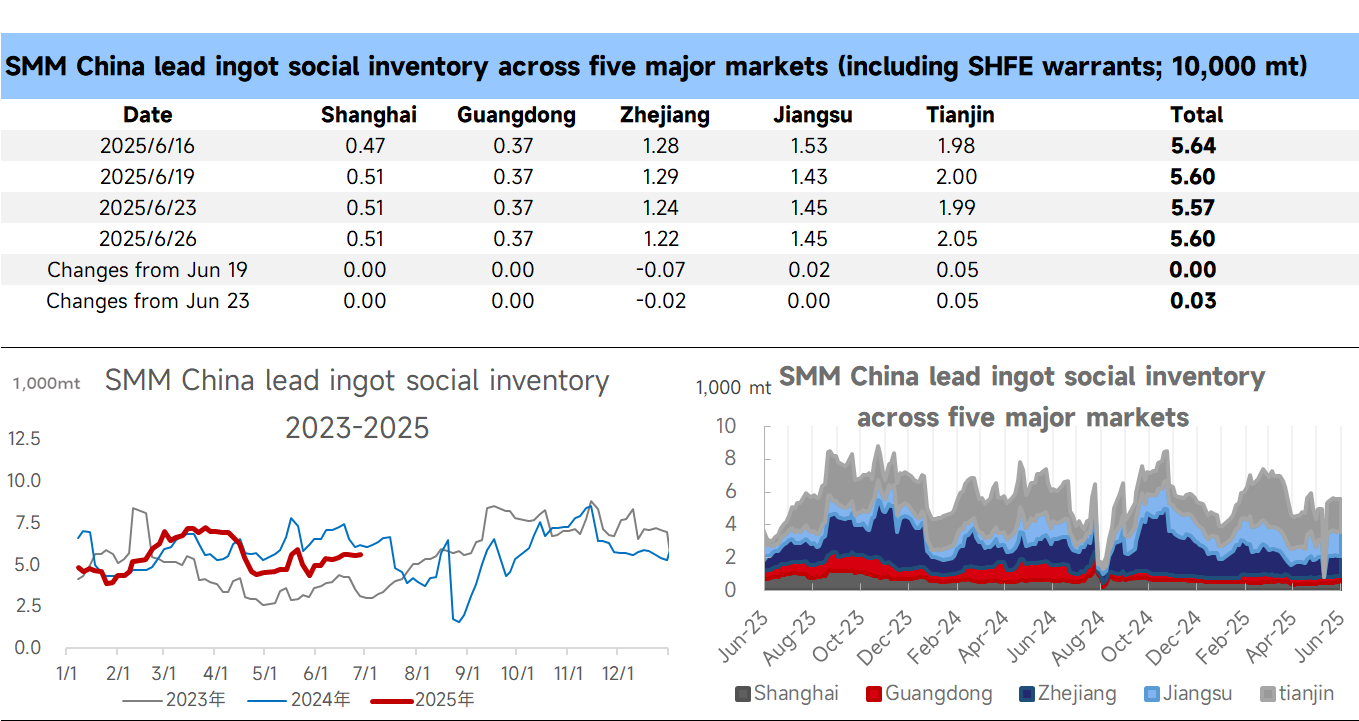

SMM News on June 26: According to SMM, as of June 26, the total social inventory of lead ingot in five regions reached 56,000 mt, unchanged from June 19 and up by over 300 mt from June 23.

This week, lead prices fluctuated upward and surged past the 17,000 yuan/mt threshold, with the most-traded SHFE lead contract reaching 17,255 yuan/mt, the highest level in nearly three months. Amid the rising lead prices, suppliers were actively quoting and shipping goods. Quotations in the Jiangsu, Zhejiang, and Shanghai regions were at discounts of 50-10 yuan/mt against the SHFE lead 2507/2508 contracts. Meanwhile, lead smelters' shipping enthusiasm increased, with quotations in major production areas ranging from discounts of 50 yuan/mt to premiums of 50 yuan/mt against the SMM 1# lead average price for ex-factory delivery, and discounts of 250-180 yuan/mt against the SHFE lead 2508 contract. From the supply and demand structure perspective, most primary lead smelters underwent maintenance this week, while secondary lead enterprises gradually recovered from losses, with increased willingness to resume production. On the consumption side, some large downstream enterprises were in the mid-year account closing and inventory checking period, with low demand for spot orders. Other small and medium-sized enterprises saw relatively improved purchasing sentiment as lead prices rose, preferring cargoes self-picked up from production sites. Overall, supply and demand were in a relatively balanced state, having little impact on social inventory. Additionally, we need to pay attention to the subsequent resumption of production by secondary lead enterprises, as well as the impact of the expanding spread between futures and spot prices of lead, the increased willingness of suppliers to transfer to delivery warehouse, and the impact of delivery brand inventory transfers on social inventory.